Special Report: Diagnostics Year in Review 2023

Special Report: Diagnostics Year in Review 2023

Volume 9, Issue 12 | March 21, 2024

Diagnostics Year in Review 2023

If you are in the diagnostics field, you know that we are with patients at the toughest times of their lives - when they are waiting for and then receiving their diagnosis and / or prognosis. But the importance of what we do is often not recognized and appreciated. Best case - diagnostics are taken for granted. Worst case - the test results are second-guessed or overlooked.

As we look back at 2023, we see that it was a tough year for most in the diagnostic industry.

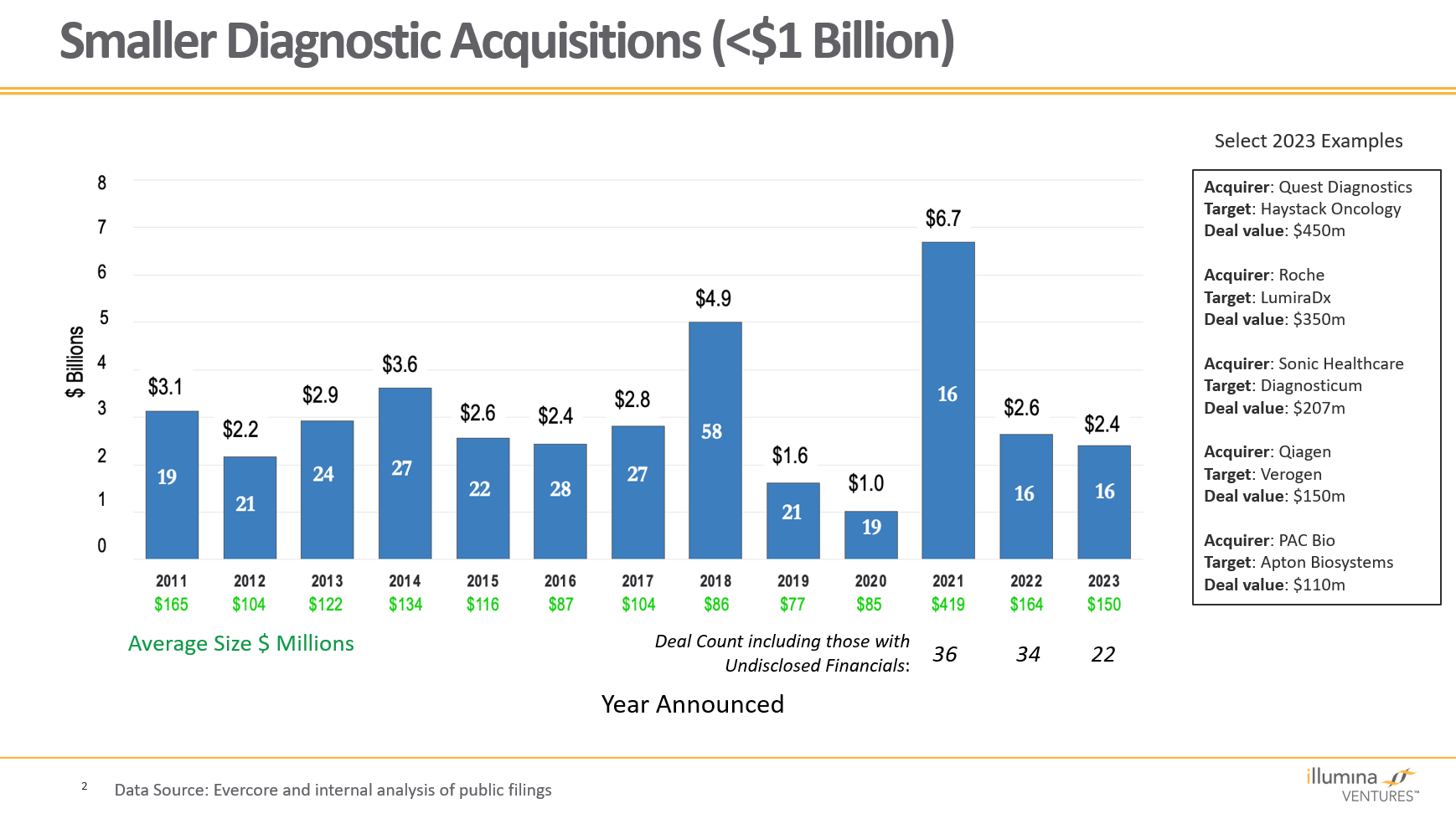

The year brought little joy financially, with the MEGA Dx Stock Index down 9% since 2020. There were no IPOs and no mega M&A deals, and small-acquisition pricing was down.

In the US, we see the threat (opportunity?) of a new regulatory regimen. Meanwhile the EU’s stricter test approval rules continue to be implemented.

Overall testing volume is flat with the exception of molecular and genomic testing.

We do see bright spots, however:

15 states passed “biomarker mandate” bills requiring payors to cover all biomarker tests under certain conditions. Ten more have bills pending. Most require tests to be FDA approved and / or the standard of care based on industry guidelines. While tests must be reimbursed, the reimbursement rate is not mandated.

Diagnostic information and commercially available tests relating to cancer and neurodegenerative diseases is expanding.

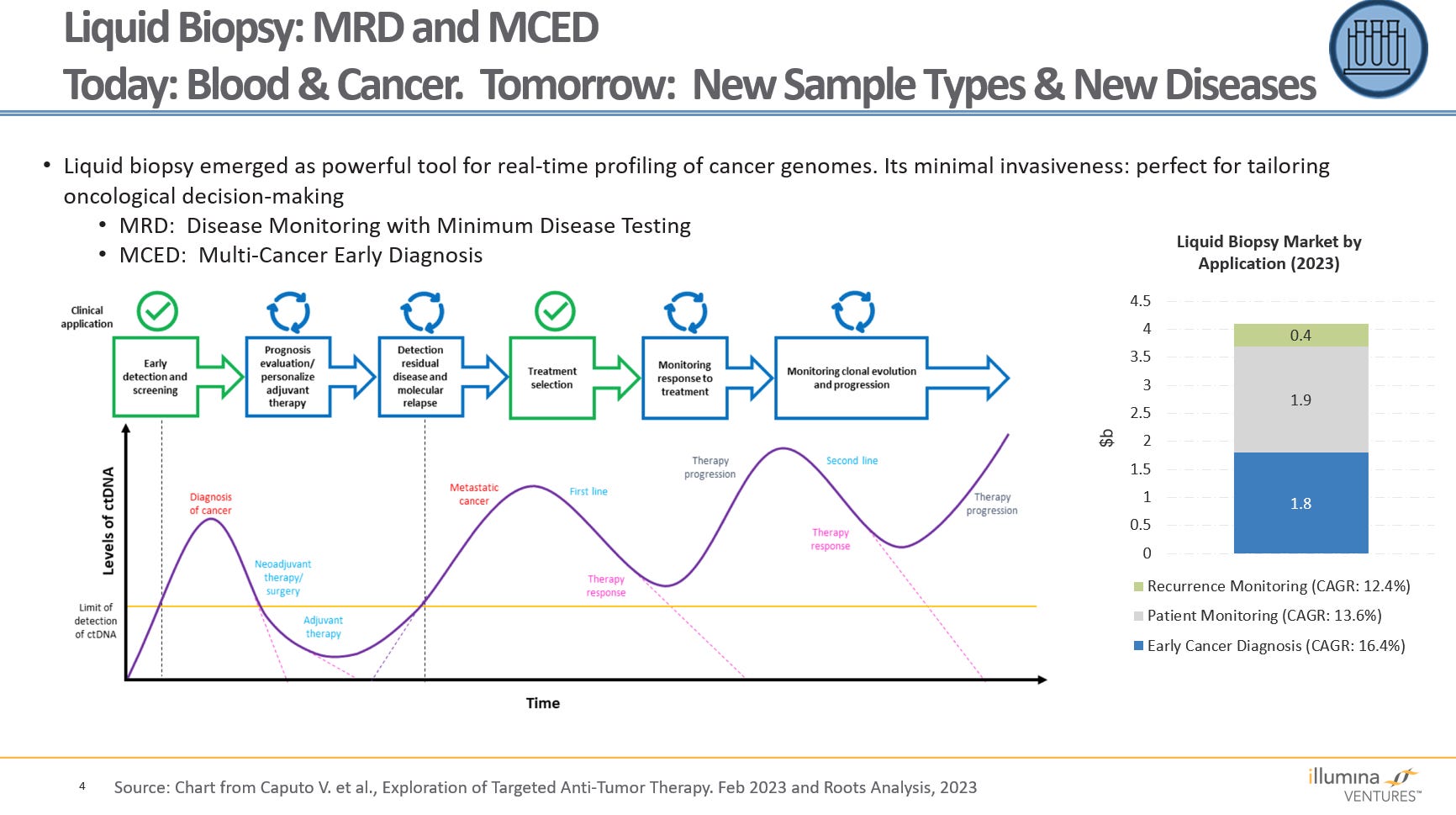

Liquid biopsy as a technology has expanded and begun to see significant adoption. Several companies now offer their own tests in two areas:

Minimal Residual Disease (MRD) tests are being widely used for monitoring cancer remission.

Multi Cancer Early Diagnosis tests (MCEDs) have gained momentum but still have a long way to go for broad acceptance. Virtually all of the uses today are in cancer, but we expect to see expansion into additional disease areas in the future. Within cancer we also expect to see more early detection tests focused on one cancer rather than a basket of different cancers.

New sample types are exploding, most of them enabling less-invasive testing methods. We believe that this is important for three reasons.

Easier and faster sample-taking means more physicians and patients will participate in point-of-care testing.

Simpler collection means that more tests can move to self collection and fully integrated self testing, growing the OTC / home-testing market.

Eventually, we expect the fully loaded cost of testing to decrease.

One overarching theme is the need for education about diagnostics. As we have covered here in the past, too many doctors, nurses, and others do not have the knowledge or experience to use tests and test results in the most appropriate way. This causes unnecessary waits and, not infrequently, harm to patients. Education also needs to extend up the value chain: Payors need to know the value of tests and be willing to pay appropriately for them.

Another big theme: Home tests are here to stay, and the healthcare industry as a whole needs to figure out how to integrate them into care. We believe that COVID was the great “legitimizer” for these, and that many (most?) Americans want their health information on their own schedule, not their doctor’s. Assuming the technology works and the FDA continues to allow tests on the market, (note: the second EUA for a flu / COVID test went through last month), the key question will be affordability and reimbursement by insurers. (Will these tests at least be FSA-eligible?) But before widespread adoption happens, more questions remain:

How can doctors be convinced to trust and use home test results for treatment decisions? (We fully understand that retesting is sometimes medically appropriate - even for lab-run tests. But not always.)

What’s the best way to document these home tests in medical records?

As home-test technology continues to develop and mature, we can no longer think of patients as people on whom tests are done - we are all now active participants in our own testing.

Lastly, the accelerated pace of innovation holds great potential for diagnostics in four major areas:

Genomics becomes multi-omics

In 2000, the genome was the “language in which God created life.” Now we know that the genome is more a toolbox than a blueprint. Multi-omics recognizes that there is a lot more we need to understand. For instance:

How mRNA is transcribed in this cell in this tissue at this time (transcriptomics)

Which proteins are translated as a result (proteomics)

The processes that invoke or repress gene expression (epigenomics)

The state of the cell (metabolomics) and its chromosomes (fragmentomics)

The trillions of our symbiotic fellow-travelers (microbiomics)

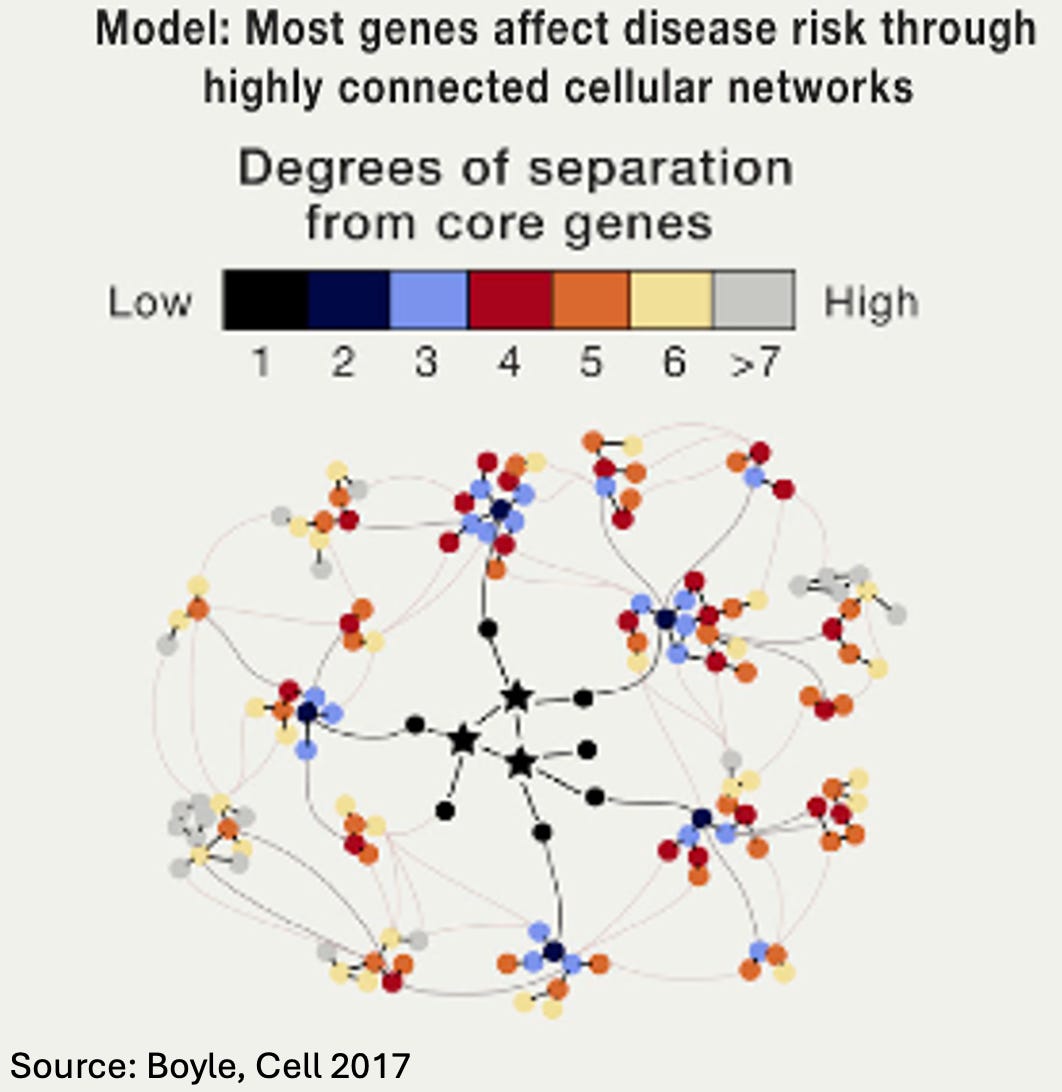

The search for specific genes that cause specific diseases has had remarkable successes, but that phase is now over. Disease may center around a few core genes active in a tissue, but these genes rarely account for more than 10% of the result. They act within a broad network of complementary, interacting, and/or regulating genes. (To root around in the weeds, see this 2017 Omnigenics Cell paper - chart duplicated here - and this 2024 paper on cancer multi-omics.)

The inexorable march of AI

AI will impact every aspect of the diagnostic process. It promises to integrate pretty much everything we know into a more personalized differential diagnosis than any single human could create. While most current applications are still one-dimensional (image analysis, cardiac rhythm, etc.), the possibility of AI systems becoming insightfully multimodal for multiple test technologies in diverse populations is there. We’re taking baby steps now, but as every parent knows, toddling turns into running in a blink of an eye.

Liquid biopsies expand beyond blood and beyond cancer

High-throughput, high-sensitivity, lower-cost techniques now enable the detection of DNA, RNA, proteins, and other materials diluted in fluids (amniotic fluid, blood/plasma, urine) or gasses (breath, sweat) at concentrations that until recently would have been impossible. Even better, these techniques are less invasive, thereby encouraging uptake. Liquid biopsy has two major uses today: MRD (Minimal Residual Disease) and Cancer Early Detection (CED). Many challenges remain (e.g., not all tissues reliably shed circulating tumor DNA (ctDNA), and the earlier the tumor stage the less ctDNA is shed, so currently available tests don’t work well for screening).

Less invasive sample types

More and more non-traditional markers of disease presence or stage are becoming predictively useful (e.g., early gait changes for Parkinson's, ease of swallowing for Alzheimer’s, skin flushing patterns for heart irregularities). AI is becoming especially useful for discovering these proxy markers for disease. Once we understand them even better, that will enable much simpler diagnostic techniques that complement or perhaps even replace more complex diagnostics.

The Diagnostics Year in Review 2023 is available at this link.